The new report State of Agtech Investment in Africa 2025 by Briter shows that both total funding and deal activity declined last year, the first such drop since tracking began. This contrasts with the broader African startup ecosystem, where funding and deal flow increased year-on-year, suggesting that agritech has stabilised at a lower baseline.

The study, which draws on data from the AgBase platform, shows that total investment fell to just under USD 170 million, down around 20% from USD 200 million in 2024, while the number of deals declined by about 10%.

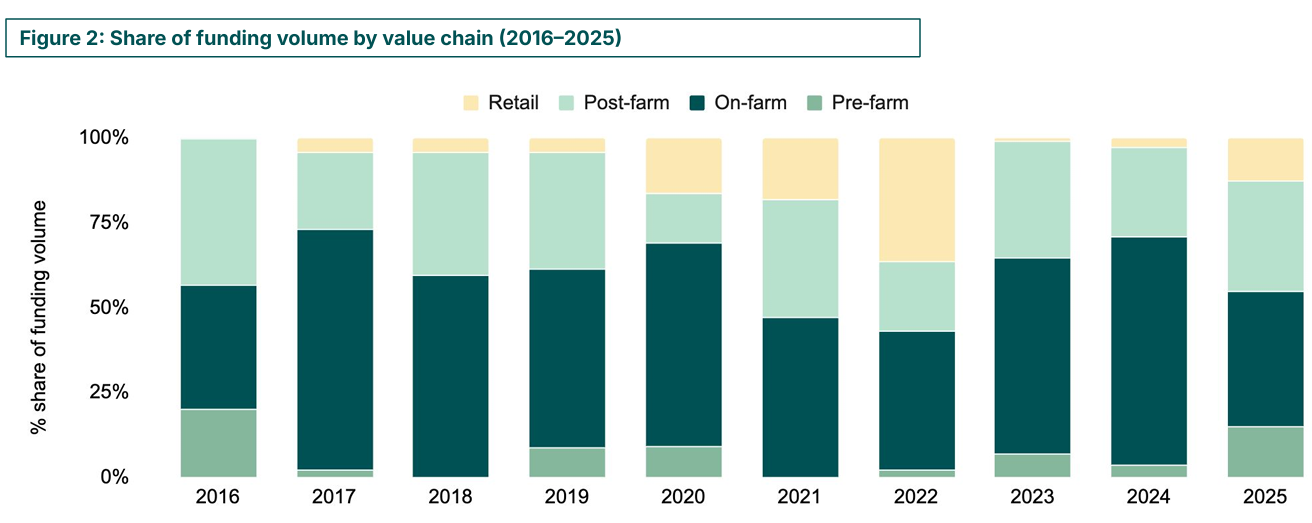

The sharpest drop was in on-farm solutions targeting smallholder farmers. In contrast, pre-farm (e.g. inputs, biotech), post-farm (processing, storage, logistics) and retail segments (distribution and delivery) all saw increased funding.

Source: AgBase 2026

What this shows is that while most deals are still in on-farm solutions (around 50%), often backed by grants, most of the money is going elsewhere. Larger funding is flowing into logistics, aggregation, marketplaces and infrastructure models that can absorb bigger tickets. Much of this is driven by debt financing in production and transport, pointing to a shift toward more asset-heavy businesses with clearer, more predictable revenues.

The importance of embedding financial services

Around a quarter of agritech companies now embed financial services, including payments, credit, insurance and equipment leasing, into their core offering. While they represent roughly 25% of companies, they account for over 60% of total funding.

This reflects a broader shift: the main constraint to scaling agriculture in Africa is often not technology, but access to working capital and financial services. As a result, capital is moving toward models that integrate financing with operations, particularly in downstream segments such as marketplaces, aggregation and logistics.

Concentration remains, but geography is widening

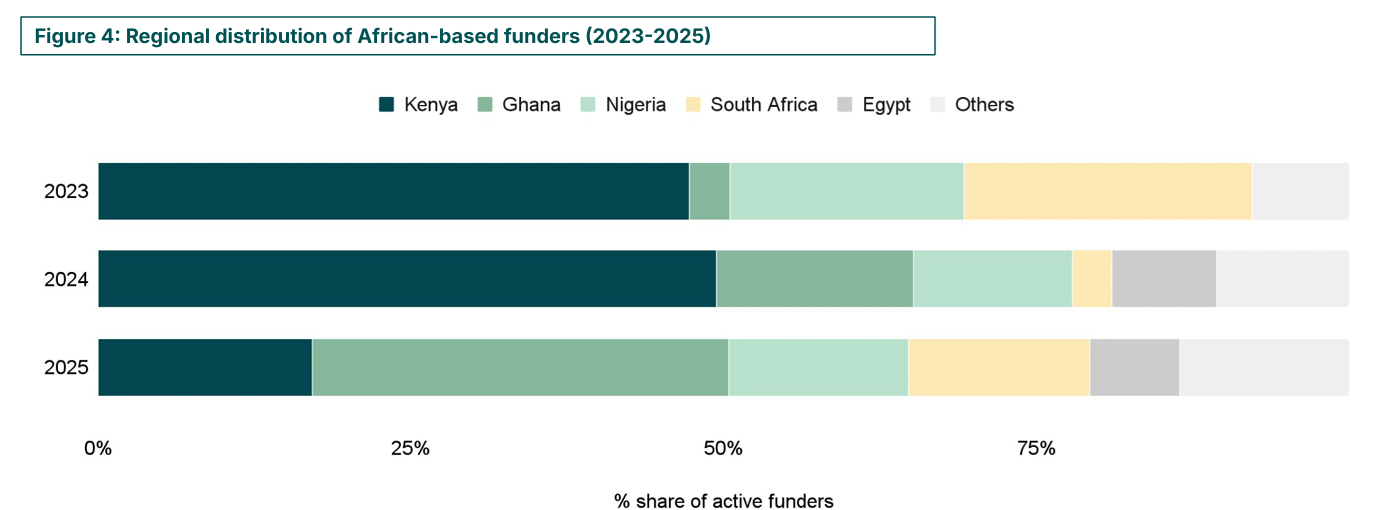

Funding remains highly concentrated. Since 2016, just 12 companies (fewer than 2% of the total) have raised over USD 50 million each and captured more than half of all agritech funding. These are primarily based in Kenya, Egypt and Nigeria, with companies such as Apollo Agriculture and Pula among the most prominent.

At the same time, the geographic spread is evolving. Kenya’s share of funding fell from over 50% in 2023–24 to around 25% in 2025, with capital spreading to markets such as Ghana, Nigeria, South Africa and Tunisia.

Source: AgBase 2026

The winner does all dynamic

A small group of scale-ups continues to capture a disproportionate share of funding. Between 2016 and 2025, just 12 companies raising over USD 50 million accounted for more than half of total agritech investment, including players such as Pula, SunCulture, Twiga Foods and Apollo Agriculture.

These companies typically follow integrated models, combining inputs, logistics, marketplaces and fintech, and are increasingly positioned as finance- and infrastructure-led platforms rather than pure technology plays.

Outcomes, however, have been mixed. Capital alone has not guaranteed resilience: those that have endured built sustainable margins, controlled costs and aligned their capital structure with asset-heavy operations, while others expanded faster than their economics allowed.

AgBase is an initiative of Briter backed by the Bill and Melinda Gates Foundation and The Foreign, Commonwealth & Development Office (FCDO), and implemented in partnership with Mercy Corps AgriFin.