The new Africa Investment Report 2025 by market intelligence company Briter shows that agritech funding in Africa remains constrained despite a broader recovery in venture activity. While African startups disclosed USD 3.8 billion in funding in 2025, fewer than 5% of deals exceeded USD 50 million, yet these accounted for around half of total disclosed funding, underscoring growing capital concentration at the top end of the market.

Briter’s data indicate that agritech continued to attract a relatively small share of capital compared with fintech and climate-focused infrastructure. In 2025, agritech funding declined further as deal volumes remained broadly stable but total capital fell and median deal sizes compressed. Investors increasingly shifted away from on-farm solutions toward post-farm, value-chain-oriented models such as marketplaces, logistics, processing and warehousing.

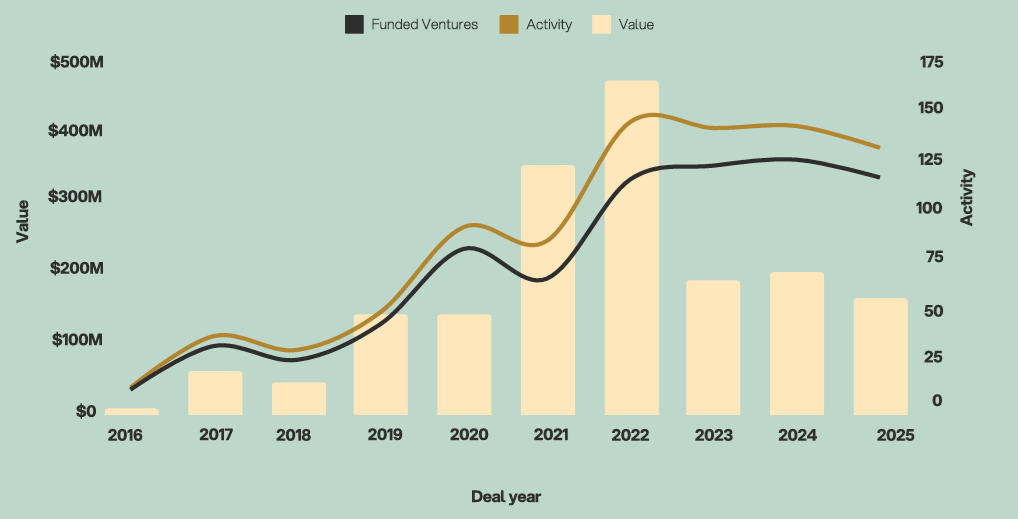

Agritech investment trends, 2016-2025

Source: Briter

These asset-heavy, revenue-backed segments accounted for nearly 50% of all agritech funding in 2025, up from just over one-quarter in 2024. This shift has been accompanied by a rise in debt financing to nearly one-third of total capital invested, leaving many early- and mid-stage agritech ventures undercapitalised and reliant on small rounds rather than progressing to growth-stage financing.

Geographically, agritech funding mirrored broader market concentration. South Africa, Kenya, Egypt and Nigeria anchored most deal value in 2025, with Kenya and South Africa particularly prominent. Deals tracked by ArisTechia included Nile’s USD 11.3 million raise and Khula’s USD 6.7 million Series A in South Africa, while in Kenya Pula Foundation raised USD 10.4 million early in the year. The second-largest reported agritech deal in Africa in 2025 was Ghana’s Complete Farmer, which raised USD 10.4 million to scale precision agriculture and market-linkage solutions.