Digital agriculture in emerging markets - 20 Mar #110

Precision AI, FMCG pivots, post-farm expansion, finance-led agritech and African investment trends

10/03/26

Verdant Impact raises $3M to scale AI-driven livestock solution

Indian agritech startup Verdant Impact has raised USD3 million in seed funding led by VC Unicorn India Ventures, to scale its digital agriculture solution Pashu.AI, strengthen R&D and expand across new regions in the country.

Founded in 2020, Verdant Impact is an AI- and IoT-driven precision genetics company that builds integrated digital solutions for sustainable dairy systems. At the core of its model is Pashu.AI, which provides multilingual AI advisory for crop management, livestock care, disease detection and real-time market insights, available in more than 20 Indian languages.

Image credit: Verdant Impact

The platform enables farmers to monitor livestock health, improve breeding decisions and manage herds using real-time data, supported by IoT-enabled tools for continuous tracking. Verdant Impact reports having served over 600,000 farmers to date and is targeting approximately USD 12 million revenue by 2026.

Why it matters

Solutions like Pashu.AI go offer unique value because they go beyond basic advisory, supporting health diagnostics, nutrition management and breeding decisions through real-time data and AI models.

The fact that the platform operates in more than 20 Indian languages shows a focus on usability and farmer adoption. The key question is whether this level of scientific precision can consistently translate into trusted, yet simple and actionable on-farm dvisory at scale.

14/03/26

WayCool raises $22.5M to strengthen supply chain and FMCG pivot

Indian agritech startup WayCool has raised INR2.1 billion (USD 22.5 million) from impact investor Lightrock, marking its first significant equity round in nearly four years.

Founded in 2015, WayCool operates a full-stack “soil-to-sale” platform, connecting over 85,000 farmers to retailers and institutional buyers. The company spans sourcing, distribution and food processing, and sells products under brands such as Madhuram and KitchenJi.

The funding comes after a period of restructuring, including layoffs and leadership changes. In FY23, WayCool reported revenue of around USD 150 million but loss were at around USD 82 million), highlighting the challenges of scaling supply chain-led agritech models.

In response, the company has been shifting toward higher-margin segments, particularly FMCG and branded products. The fresh capital is expected to support this transition, alongside strengthening its supply chain infrastructure.

Why it matters

WayCool’s latest funding reflects broader consolidation in India’s agritech sector, one of the most developed globally. Recent moves, including Arya.ag raising around USD 80 million, AgroStar securing USD 30 million, and the Unnati–Gramophone merger, point to a stronger focus on scale and more sustainable business models. In particular, WayCool’s pivot toward FMCG highlights a wider shift toward downstream, post-farm segments, where margins are higher and revenue streams more predictable.

17/03/26

Lersha and EABC target 1 million Ethiopian farmers with finance, inputs and mechanisation

Ethiopian agritech Lersha and the Ethiopian Agricultural Businesses Corporation (EABC), a federal government public enterprise, have signed a Memorandum of Understanding aimed at reaching 1 million smallholder farmers with access to finance, agricultural inputs and mechanisation services by 2030.

Image credit: Lersha

The partnership combines Lersha’s digital platform with EABC’s machinery and input supply network, enabling service delivery through integrated physical supply chains. It is aligned with national initiatives including the National Agri-Finance Implementation Roadmap (NAFIR), the Digital Agriculture Roadmap (2025–2032) and the National Mechanization Strategy.

Founded in 2018, Lersha uses a phy-gital model connecting 270,000+ smallholder farmers, and 250+ service providers, offering a marketplace for agricultural inputs, mechanization, access to finance, market linkage, agro-climate advisory and fertilizer recommendation through both online and offline solutions. For service delivery, the agritech leverages a network of 2,000+ agents, a call center (7860), and the Lersha digital platform.

Since March 2023, the company has worked with the Ethiopian Agricultural Transformation Institute (ATI) to develop digital profiles for over one million farmers, enabling fertiliser recommendations and climate-informed advisory.

Why it matters

Ethiopia’s Digital Agriculture Roadmap (2025–2032) places credit and insurance at the centre of its scale-up strategy, but delivery has remained fragmented. By linking farmer data, input supply and mechanisation with financing, this partnership is a test of whether those ambitions can be operationalised into a functioning, end-to-end system at scale.

18/03/26

Ghana launches Timbuktoo AgriTech Hub to scale digital agriculture

Ghana has launched the Timbuktoo AgriTech Hub in Accra, backed by the United Nations Development Programme (UNDP), as part of a broader push to scale digital innovation in agriculture.

The hub is part of the Timbuktoo initiative, a USD 1 billion pan-African programme launched by UNDP in 2024 to support impact-driven, early-stage startups. It aims to mobilise public and private capital to create 10 million jobs and impact 100 million livelihoods, while addressing gaps such as limited early-stage funding, weak incubators and fragmented markets.

The initiative is being rolled out through eight hubs (Accra, Kigali, Lagos and Nairobi) supporting sectors such as fintech, healthtech and agritech. The Ghana hub focuses on agriculture, building on the country’s wider digital agriculture agenda.

The AgriTech Hub brings together partners including 500 Global and Seedstars, and targets challenges such as fragmented supply chains, limited finance and climate risks through mobile technologies, data-driven tools and AI. In practice, the hub will operate as both an innovation and financing platform, offering incubation, access to capital, pan-African networks and capacity-building support.

Why it matters

This reflects a shift from fragmented startup support toward more coordinated, continent-scale innovation platforms. As agritech funding becomes more constrained and innovation spreads across a wider set of markets (see below analysis article), there is a growing need for knowledge sharing, coordination and cross-continental collaboration, besides capital.

05/03/26

Analysis - African agritech funding slows as capital shifts downstream and toward finance-led models

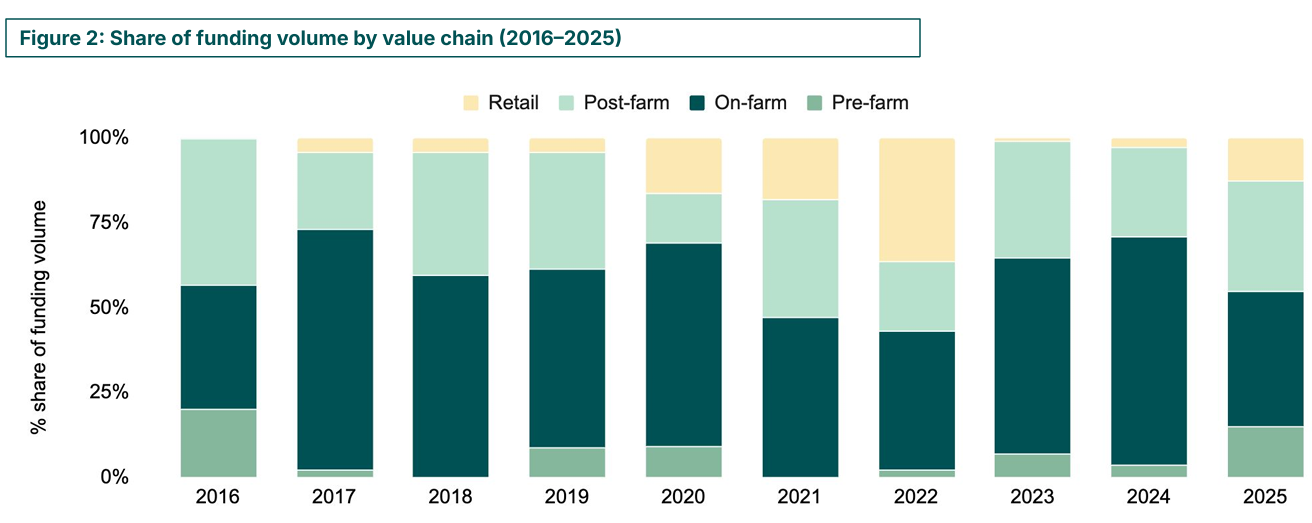

The new report State of Agtech Investment in Africa 2025 by Briter shows that both total funding and deal activity declined last year, the first such drop since tracking began. This contrasts with the broader African startup ecosystem, where funding and deal flow increased year-on-year, suggesting that agritech has stabilised at a lower baseline.

The study, which draws on data from the AgBase platform, shows that total investment fell to just under USD 170 million, down around 20% from USD 200 million in 2024, while the number of deals declined by about 10%.

The sharpest drop was in on-farm solutions targeting smallholder farmers. In contrast, pre-farm (e.g. inputs, biotech), post-farm (processing, storage, logistics) and retail segments (distribution and delivery) all saw increased funding.

Source: AgBase 2026

What this shows is that while most deals are still in on-farm solutions (around 50%), often backed by grants, most of the money is going elsewhere. Larger funding is flowing into logistics, aggregation, marketplaces and infrastructure models that can absorb bigger tickets. Much of this is driven by debt financing in production and transport, pointing to a shift toward more asset-heavy businesses with clearer, more predictable revenues.

The importance of embedding financial services

Around a quarter of agritech companies now embed financial services, including payments, credit, insurance and equipment leasing, into their core offering. While they represent roughly 25% of companies, they account for over 60% of total funding.

This reflects a broader shift: the main constraint to scaling agriculture in Africa is often not technology, but access to working capital and financial services. As a result, capital is moving toward models that integrate financing with operations, particularly in downstream segments such as marketplaces, aggregation and logistics.

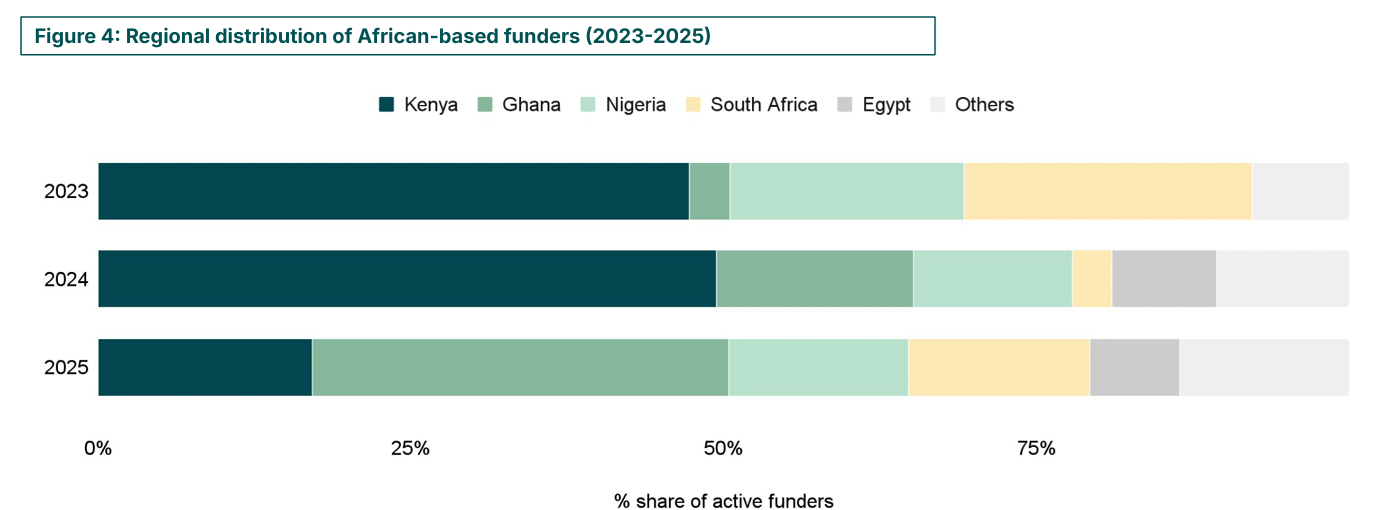

Concentration remains, but geography is widening

Funding remains highly concentrated. Since 2016, just 12 companies (fewer than 2% of the total) have raised over USD 50 million each and captured more than half of all agritech funding. These are primarily based in Kenya, Egypt and Nigeria, with companies such as Apollo Agriculture and Pula among the most prominent.

At the same time, the geographic spread is evolving. Kenya’s share of funding fell from over 50% in 2023–24 to around 25% in 2025, with capital spreading to markets such as Ghana, Nigeria, South Africa and Tunisia.

Source: AgBase 2026

The winner does all dynamic

A small group of scale-ups continues to capture a disproportionate share of funding. Between 2016 and 2025, just 12 companies raising over USD 50 million accounted for more than half of total agritech investment, including players such as Pula, SunCulture, Twiga Foods and Apollo Agriculture.

These companies typically follow integrated models, combining inputs, logistics, marketplaces and fintech, and are increasingly positioned as finance- and infrastructure-led platforms rather than pure technology plays.

Outcomes, however, have been mixed. Capital alone has not guaranteed resilience: those that have endured built sustainable margins, controlled costs and aligned their capital structure with asset-heavy operations, while others expanded faster than their economics allowed.

AgBase is an initiative of Briter backed by the Bill and Melinda Gates Foundation and The Foreign, Commonwealth & Development Office (FCDO), and implemented in partnership with Mercy Corps AgriFin.

19/03/26

Good reads - FAO examines the state of insurtech in agriculture

A new FAO report Leveraging digital innovation to promote agricultural insurance among small-scale farmers highlights how digital technologies are beginning to transform one of the most underdeveloped segments of rural finance: agricultural insurance.

Despite its importance for climate resilience, coverage remains extremely low. Only around 19% of smallholders globally are insured, with penetration in sub-Saharan Africa below 3%. High costs, weak data systems and limited distribution have long made these products difficult to scale.

The report argues that digital technologies are starting to address these structural constraints, but unevenly. Mobile platforms have already played a key role in reducing distribution costs and enabling bundled models, where insurance is offered alongside inputs, credit or advisory. In Kenya, for example, platforms like DigiFarm integrate insurance from providers such as Pula and ACRE Africa into broader service ecosystems.

Recent tech innovation is focused on data and risk modelling. Satellite imagery, drones and telecom data (e.g. commercial microwave links, or CMLs, which use mobile network signals to measure rainfall) are improving loss assessment and generating more granular weather data, while AI is enhancing risk profiling and pricing.

There are also early examples of farmer-generated data. Picture-based insurance pilots allow farmers to upload images of their fields via mobile apps, improving loss verification and reducing basis risk.

Together, these advances are making agricultural insurance more accurate and affordable. However, scale remains limited. Most models still rely on bundling, partnerships and subsidies, and are concentrated in markets with stronger digital ecosystems like East Africa.

The result is a familiar pattern: strong innovation at the edges, but limited system-wide scale. Closing the insurance gap will require not just better technology, but stronger integration across finance, distribution and public systems.