Digital agriculture in LMICs - 23 Jan #105

Agritech funding tightens as telcos invest in satellite-enabled rural connectivity

14/01/26

Indonesia tech funding down 38% after agritech scandals

According to a recent report by market intelligence firm Tracxn, tech startup funding in Indonesia declined by 38% year-on-year in 2025, with reduced capital deployment across seed, early-stage and late-stage rounds as investor scrutiny increased.

The funding slowdown followed a series of high-profile controversies in agritech and aquatech, sectors that had previously attracted substantial venture capital. AquaTech eFishery faced governance and financial irregularities during 2024–25, while agricultural commerce platform TaniHub came under investigation after its lending arm, TaniFund, was ordered to shut down in April 2024 over allegations that venture capital funds were used to cover loan defaults. Indonesia accounted for 58% of Southeast Asia’s agritech funding in 2024, based on ArisTechia analysis.

At the same time, Tracxn data shows that food and agriculture technology was the top-funded tech segment in Indonesia in 2025, despite the broader funding contraction and recent agritech controversies. The sector raised USD 70.6 million, up 72% from 2024, reflecting continued investor focus on infrastructure-linked models supporting production systems, logistics and farm-level services, even as funding remained well below the USD 280 million recorded in 2023.

15/01/26

Safaricom refines DigiFarm strategy around Kilimo and Soko

In a recent press release and YouTube video featuring remarks from DigiFarm Director Seema Gohil, Kenyan mobile operator Safaricom has clarified how it positions its agritech platform DigiFarm, explicitly framing it as two new integrated tools, Kilimo and Soko, that together will anchor its core value proposition.

Photo credit: Safaricom

While DigiFarm has long combined digital advisory, input financing and market linkages, recent updates place clearer emphasis on Kilimo as the agronomy, training and finance layer, and Soko as the marketplace connecting farmers to buyers, cooperatives and processors, supported by digital records and M-PESA payments. The articulation underscores Safaricom’s focus on linking productivity support with an end-to-end agricultural value-chain approach, rather than treating finance and advisory as standalone interventions.

That approach is reflected in the recent launch of Jipange Cash Advance, a short-term liquidity facility for tea farmers developed with Access Bank Kenya and local tea agribusinesses. By advancing funds against verified tea deliveries and automating repayment once factory payments are completed, Jipange directly ties financing to value-chain participation. The product has been piloted across four tea factories in the Rift Valley, with plans to scale nationally and expand to other value chains.

15/01/06

Indonesia’s Beleaf raises fresh capital in extension of Series A round

Indonesian agritech Beleaf has raised undisclosed fresh capital, estimated to be close to USD 1 million, according to DealStreetAsia. The funding was structured as a convertible note (a form of debt that converts into equity at a later date), and was backed by Openspace Capital, alongside a group of angel investors and company founders.

The new capital represents an extension of Beleaf’s August 2023 Series A round, in which the company raised USD 6.85 million to scale its farming as a service (FaaS) model, under which it provides farmers with inputs, agronomy support, technology, and post-harvest, logistics, and offtake services. That round was followed by an additional USD 3.5 million extension in August 2024, bringing total post-Series A funding to more than USD 10 million.

Alongside the fresh investment, Beleaf is reportedly reducing its workforce as part of a broader effort to improve operational efficiency and move toward profitability in 2026. The company, which operates a B2B2C agritech model, working directly with farmers while supplying produce into downstream consumer markets, plans to deploy the new funds to onboard more farmers and expand its total area of farmland.

Founded in 2019, Beleaf initially began as a hydroponic farming operation before evolving into a technology-enabled agribusiness focused on improving productivity and yields for smallholder farmers. The company leverages big data and Internet-of-Things (IoT) technologies to deliver precision farming, automation, and farm management services.

17/01/26

Kenya and IFAD launch EU-funded digital ag and soil health programme

A new three-year initiative has been launched in Kenya in partnership with the national and county governments to advance digital agriculture and soil health. The KSH 600 million (USD 4.64 million), EU-funded programme, implemented with the International Fund for Agricultural Development (IFAD), targets 40,000 smallholder farmers across six counties.

Known as Investing in Livelihood Resilience and Soil Health (ILSA), it builds on the Kenya Cereal Enhancement Programme–Climate Resilient Agricultural Livelihoods launched in 2015, which introduced digital e-vouchers for farm inputs and advisory services. The programme supports integrated soil fertility management, climate-smart agriculture and post-harvest handling, anchored by a digital e-voucher platform linking farmers to private-sector providers and embedded within county systems to ensure sustainability beyond the grant period.

Analysis

20/01/26

Philippines’ telcos move toward direct-to-cell satellite for rural coverage

Philippine mobile operators are advancing direct-to-cell and direct-to-device satellite connectivity, as Globe Telecom partners with Starlink, while Lynk Global conducts early satellite-to-phone trials with the other major telco Smart. The technology allows standard LTE (4G) smartphones to connect directly to low-Earth-orbit satellites beyond the reach of terrestrial mobile networks.

Under its agreement with Starlink, Globe plans to integrate direct-to-cell satellite services into its mobile network to extend coverage to remote islands and underserved rural areas across the Philippines. As an archipelago of more than 7,600 islands, the country faces structural challenges in achieving nationwide mobile coverage using terrestrial infrastructure alone, positioning satellite-enabled connectivity as a strategic complement rather than a replacement for existing networks.

Photo credit: Developing Telecoms

In parallel, Lynk Global has carried out direct-to-device testing with Smart Communications, including trials in Catanduanes, demonstrating basic messaging and limited data capabilities in areas without cellular coverage. The tests form part of broader preparations for potential commercial satellite-to-mobile services in the country.

Why it matters

Agriculture is among the sectors expected to benefit most from improved connectivity, particularly in rural regions where farmers and agribusinesses face persistent coverage gaps. Many digital agriculture applications are designed to operate with limited bandwidth, but more reliable satellite-enabled connectivity would support wider adoption across remote farming communities.

The Philippine initiatives reflect a broader global trend, as mobile operators increasingly partner with satellite providers to extend coverage, improve network resilience, and advance digital inclusion beyond traditional terrestrial footprints. In Africa, as reported by ArisTechia, mobile operator Airtel recently announced a partership with Starlink to rollout direct-to-cell satellite connectivity across 14 countries, beginning in 2026.

20/01/26

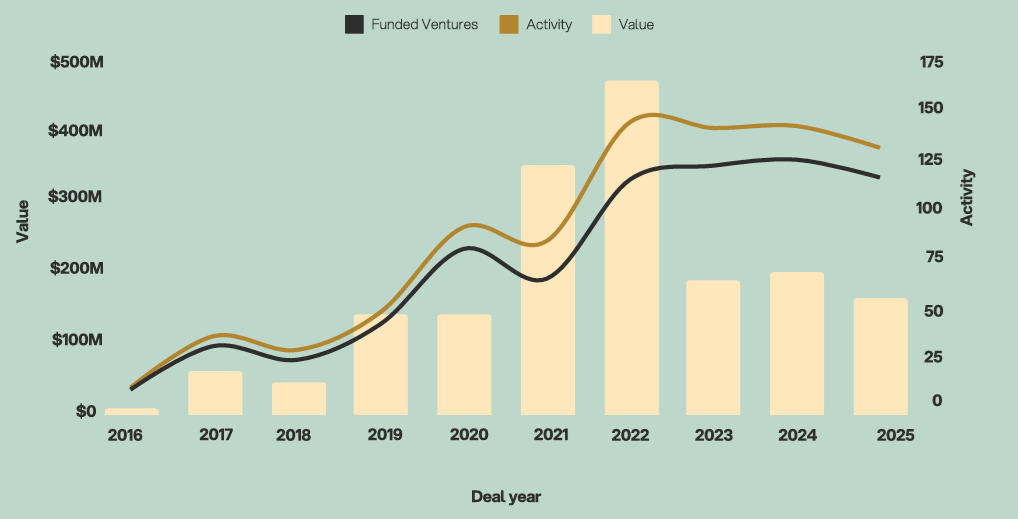

African agritech funding lags as capital concentrates in larger deals

The new Africa Investment Report 2025 by market intelligence company Briter shows that agritech funding in Africa remains constrained despite a broader recovery in venture activity. While African startups disclosed USD 3.8 billion in funding in 2025, fewer than 5% of deals exceeded USD 50 million, yet these accounted for around half of total disclosed funding, underscoring growing capital concentration at the top end of the market.

Briter’s data indicate that agritech continued to attract a relatively small share of capital compared with fintech and climate-focused infrastructure. In 2025, agritech funding declined further as deal volumes remained broadly stable but total capital fell and median deal sizes compressed. Investors increasingly shifted away from on-farm solutions toward post-farm, value-chain-oriented models such as marketplaces, logistics, processing and warehousing.

Agritech investment trends, 2016-2025

Source: Briter

These asset-heavy, revenue-backed segments accounted for nearly 50% of all agritech funding in 2025, up from just over one-quarter in 2024. This shift has been accompanied by a rise in debt financing to nearly one-third of total capital invested, leaving many early- and mid-stage agritech ventures undercapitalised and reliant on small rounds rather than progressing to growth-stage financing.

Geographically, agritech funding mirrored broader market concentration. South Africa, Kenya, Egypt and Nigeria anchored most deal value in 2025, with Kenya and South Africa particularly prominent. Deals tracked by ArisTechia included Nile’s USD 11.3 million raise and Khula’s USD 6.7 million Series A in South Africa, while in Kenya Pula Foundation raised USD 10.4 million early in the year. The second-largest reported agritech deal in Africa in 2025 was Ghana’s Complete Farmer, which raised USD 10.4 million to scale precision agriculture and market-linkage solutions.

Good reads (what ArisTechia is reading..)

16/01/26

PxD and BCG highlight delivery gap in national-level digital ag initiatives

Precision Development (PxD), a global nonprofit organisation that supports smallholder farmers, and Boston Consulting Group (BCG) have published a new report arguing that the biggest constraint in digital agriculture is no longer strategy, but delivery. The study titled From Strategy to Scale: Why Delivery Matters in Digital Agriculture identifies Digital Agriculture Units (DAUs) as the missing institutional link between national digital roadmaps and measurable outcomes for farmers.

Despite rapid growth in tools such as SMS advisory services, IVR systems, and digital farmer registries, smallholder adoption remains below 15% globally, while public spending on agricultural digital infrastructure represents just 2% of total agricultural expenditure in OECD countries. The report describes a persistent “strategy-to-delivery gap”, where pilots multiply but scale and impact stall.

Drawing on experience from Ethiopia and India’s Odisha state, PxD and BCG show how DAUs embedded within governments translate roadmaps into costed plans, coordinate actors, and track results. In Odisha, the Krishi Samruddhi programme reaches 7.9 million farmers at USD 0.15 per farmer, cutting severe crop losses by 10% and pest losses by 26%.

The authors estimate digital agriculture could unlock up to USD 500 billion annually in additional agricultural GDP, if governments invest in delivery capacity as seriously as vision.