A look at 2023 trends in agritech funding #42

At the start of the year, it is time to dig deep into the AgrisTechia archives for some analysis on 2023 trends in digital agriculture in LMICs

In this special Friday edition, I share some highlights on agritech reported deals and funding across our key focus regions: Africa, South Asia and Southeast Asia.

Going forward, I will aim to post more of these aggregated insights and analysis, leveraging our weekly reporting on digital agriculture news. I hope you like it, and as always your feedback is very much welcome.

How much money was raised in 2023?

In the past year, AgrisTechia’s weekly reporting tracked a total of USD 564 million investment in agritech start-ups across the three regions. This sum covers all the reported raises in agritech startups that focus on smallholder agriculture. The 564 million is the result of a total of 56 reported deals, including a variety of funding mechanism such as grants, debt and equity financing. In addition, we tracked 6 undisclosed deals.

This is how the picture looks like, when looking at the distribution of funding by regions over the year.

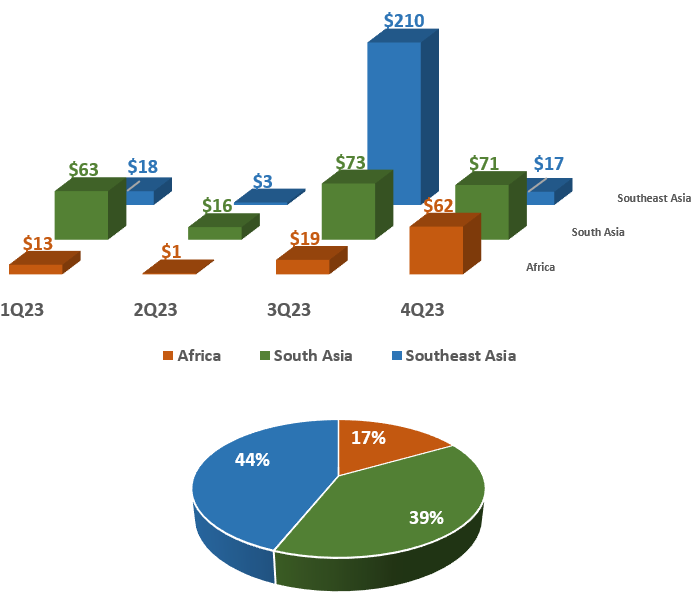

Fig. 1: Agritech funding by region in 2023 ($ million)

Source: AgrisTechia

Now, looking at where the money went and at the overall trend, agritech funding in the three regions saw an acceleration in the third quarter, and a comparatively strong year-end, after a slow start of the year and a depleted second quarter.

Southeast Asia was the leading region, managing to beat South Asia by a small margin, with a total of $248 million raised (44% of the total), just over the $222 million raised in the South Asia region (39% of the total). However (and this is a big however) Southeast Asia’s leading position is largely explained by the huge $200 million Series D raised by Indonesian aquatech eFishery in July, which made the company reach an evaluation of $1.4 billion at the time of the announcement, becoming Indonesia’s first agritech unicorn. The raise is expected to drive international expansion for the aquatech starting from India.

By comparison, the second largest deal of the year came in September at “only” $62.5 million. It was secured in by India’s farm analytics and agri advisory company Leads Connect, followed in third place by another Indian agritech, B2B agri e-commerce Vegrow, which right at the end of the year (December) bagged $46 million.

In a challenging year characterised by an overall deceleration or “funding freeze”, Africa was trailing behind. Nonetheless African agritechs managed to raise $94 million (17% of the total for the three regions). Kenyan agritechs raised 59% of the funding for the whole Africa region (10% globally), consolidating the country’s role as a regional agritech hub and an agritech leader globally.

Notable deals in the East African country included the $9.5 million loan secured by Apollo Agriculture in February to boost African expansion, and the $35 million debt funding raised by B2B agri e-commerce Twiga Foods in November as part of a business refinancing process. Ghana follows by some distance at just over $12 million, resulting from three reported deals including $10.4M secured by Complete Farmer for its precision agriculture and market linkages solution.

What level of activity did we see over the year?

By looking at the number of reported deals quarter-by-quarter across the three regions, the picture appears more balanced, with the expected prevalence of South Asia and more specifically (and unsurprisingly) of India. Out of a total 62 reported deals tracked by AgrisTechia in 2023, 25 were in South Asia, representing 40% of the total number of deals in the three regions. Out of those 25, India took the lion’s share with 22 deals.

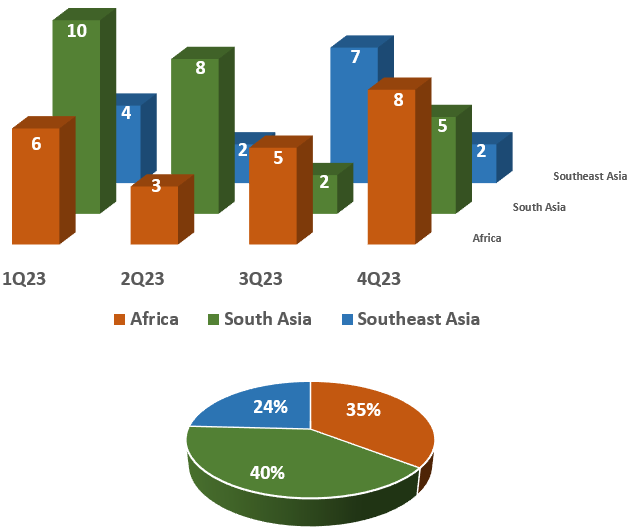

Fig. 2: Number of agritech deals by region in 2023

Source: AgrisTechia

In terms of activity, in Southeast Asia Indonesia is (also unsurprisingly) prevalent with 9 reported deals out of 15 for the region, followed by Vietnam, a fast growing market with 4 reported deals in 2023 and one to watch for 2024. The Philippines trail third for number of deals but second for amount of funding raised in the year, with two agri e-commerce platforms, Kita and Mayani, closing in the year their respective seed round.

Overall, 1Q23 was actually quite dynamic, scoring the highest number of deals by quarter (20 in total), even though the amount of funding in the first quarter was lower than in the third and fourth quarter. There were still some good ticket sizes such as the $13.5 million raised by Indonesia’s B2B e-commerce EdenFarm and the $25 million raised by Indian agri-climate tech Ecozen.

While in Africa the average ticket size is comparatively smaller, there has been some good activity across the year. What is interesting to notice is that while Kenya maintains its regional leadership (6 deals out of 22 in Africa), it is not as dominant with the region as it is India in South Asia or Indonesia in Southeast Asia. There are a few other hotspots of innovation in Africa. Besides the usual suspects, in 2023 we saw investments going into agritechs in Morocco, Liberia, Uganda and Zambia. The region is also seeing the most “multi-country deals” (five out of six tracked by AgrisTechia globally), with several startups securing investment to venture out of their home countries and expand into other regional markets.

This was the case in 2023 for OKO Insurance, which starting out of Mali, raised $250,000 for B2B expansion into Africa. TomorrowNow also raised a $5M Gates grant for climate adaptation targeting 20 million farmers across multiple East African countries, while Cavex secured $6M to scale its pan-African digital carbon financing platform.

This is a first stab at analysing and describing trends emerging from the rich data collected on an ongoing basis by AgrisTechia. There is obviously much more to explore. Going forward, I aim to publish quarterly review pieces: The next special edition will look at trends in 4Q24 VS 4Q23 in the world of agritech in LMICs.

Watch out for more news and analysis, and as usual thoughts and feedback are welcome!